Michael (Mike) has a broad and diverse background with significant commercial and strategic experience.

He is an experienced Senior Executive Manager and manages strategic leadership roles with P&L. He has substantive experience and knowledge ranging from:

• Procurement & Supply Chain

• People

• Commercial

• Legal and Contract Management

• Governance and Risk

• Engineering

• Customer Services

• Marketing

• Project and Product management;

• Managing Director growing start-up businesses

• Extensive Senior Executive management experience in multiple large complex organisations as divisional manager of in country multi-national customer centric companies.

Mike has led teams in sport from age of 11 and business from age of 24 and loves to lead through making a difference to the way in which people think, work and execute change to deliver meaningful outcomes.

He is always inspired by people doing amazing things.

He seeks to build rapport and has a history of growing loyal and highly functioning teams and creating space for ideas and confidence to develop.

Weismann has a point where he stressed that “essentially states that the pursuit of acknowledgement from the executive suite and the feeling that you are being personally and professionally disrespected if you’re not working at board level, is a fallacy”. He suggests that rather than focusing on the role of procurement in the C-suite, the main way to exert influence is still “the old-fashioned way: through performance”.

Even if you’re not at the table, Nick Verkroost talks about the importance of having a voice at the table – Through the ability to be able to influence stakeholders.

There have also been many publications about the Soft Skills required for procurement professionals. Soft Skills are defined in the oxford dictionary as “personal attributes that enable someone to interact effectively and harmoniously with other people”.

There are so many examples of what these skills are, and correlation is sometimes difficult to achieve generally. The table below is taken from the following publication and is a good general benchmark.

Soft skills are non-technical skills that describe how you work and interact with others. Unlike hard skills, they’re not necessarily something you can learn in a course, like data analytics or programming. Instead, they reflect your communication style, work ethic, and work style.

Do you agree with this? Can soft skills be taught or are we born with them?

Throughout my career, I have wondered why we put a framework / box around these skills and define them as “soft skills”. Are we not doing them a disservice and undermining how hard it is to find people that really excel with these attributes, and underplaying how difficult it is to train them? I always use the frame of “POWER skills” for that reason. What do you call them?

For procurement Professionals soft skills defined by the Chartered Institute of Procurement and Supply are.

What does this all mean? From the top 5 skills listed above and their detailed explanations, I think the key threads are the ability to build relationships through clear communications and collaboration whilst leading the engagement strongly, building successful value outcomes for all stakeholders and suppliers. A bit of a long sentence but captures the essence of above.

However, fundamental to procurement professionals and the most important attribute is the POWER to INFLUENCE!

Think about the procurement process! At a high-level – Plan / Source / Manage

As a support function, Procurement rarely owns the budget and outcome of what is purchased. When discussing with stakeholders and budget holders about procuring a product or service delivering a customer outcome; how often even at the needs analysis stage does the stakeholder have their own ideas of who can deliver the outcome?

Similarly, when performing a market analysis how often does the stakeholder know the suppliers who could deliver the outcome?

Here is where you Influence POWER starts (especially if you know there are much better and/or new and innovative suppliers in the market than the ones offered up by a stakeholder).

In very technical fields senior technical leaders have gained their reputation based on their technical knowledge – knowledge built over the course of their working life.

How do you convince a senior engineer that company x (a name not recognised in the traditional market) can produce the highest quality outcome?

So, you have analysed the market, obtained all empirical data, and presented it to the stakeholders but the engineer says, “Over my dead body!” What do you do next?

The ability to Influence is again the POWER that you need to take this individual on the journey of change. You can only influence if you have Trust with your stakeholders and that is built on relationship and delivery. This exact scenario happened to me and it took over 3 years of coaching and influencing to get a great outcome for the organisation).

Evaluation will require the Influencing POWER. When I hear you say! At panel shortlisting when you can’t get a consensus.

What are your thoughts about this statement?

The Negotiation stage is about preparation and understanding your organisations BATNAs (Best Alternative To Negotiated Outcomes), However during the process there likely will be stages where you have to use the Influence POWER to obtain some of your desired outcomes.

Management and Performance usually comprising KPI measurements and monthly meetings will also highlight opportunities where a procurement professional will have to use their Influence POWER. Especially when asking the supplier to go the extra mile to sort out an issue.

There will also be instances when you meet with stakeholders using the performance data supplied to either commence performance management, reward the supplier, or start a new sourcing process.

Our profession along with most professions today need lots of these POWER Skills and there is always plenty of debate about the priority attributes.

I hope this has helped to simplify and provided some food for thought on what a complex issue this is and helps you think about the main attribute that you need to have as a procurement professional.

A question I will leave you with: If you have the POWER of Influence as a procurement professional, then why do you need a seat at the C suite table?

My views and opinions on this vast topic are part of a much wider industry dialogue – I’d love to hear your insights and feedback too.

If you are interested here is other reading on influence Power

There is lots of talk and media attention currently around leadership/ accountability be it good or bad . At Augment Resources both here in New Zealand and in Australia we are focused at creating new and existing leaders through executive search and placement with the most exciting area is creating new leaders in the Procurement and Supply chain through are unique innovative and award winning grad program

I thought it would be timely to repost something I posted in 2021 about the key influences on my 25 years of leadership

Enjoy and if you are interested in expanding the conversation please comment and I’m certainly available for a chat

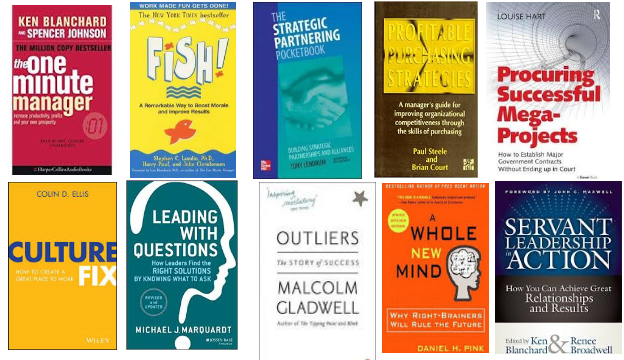

Leadership Hack – The Top 10 books that shaped my leadership career

Since the age of 18 I have been working and developing my leadership knowledge through practical experiences, professional courses, qualifications, books and the practical experience that comes from being part of a work based team. At the age of 24 I was given my first leadership role at British Telecom leading a team of over 20 people. Christmas 2020 has seen me reflect on my leadership journey and knowledge gained and implemented in many of my past teams and organisations. There are so many writers missing including Richard Branson, Sir Alex Ferguson, Jeffery Hiatt, Gwendoline Smith, Don Steinberg but I’ve selected the texts I often refer to with the most thumbed pages.

After an extraordinary year that I never thought I would experience and the impact of COVID19 I have summarised my key “takeaways” from each book. I know that when you get the chance to read some of these publications you’ll find many others. Let us kick off with the first book and enjoy.

Ken Blanchard & Spencer Johnson – the One minute manager

This book was designed for busy Managers and suggests that you spend 60 seconds per day; or at least per week (my thoughts) on each of the following;

a) Discussing and setting clear goals

b) Giving praise as feedback

c) Creating clarity and feedback when things require development (reprimands)

Basically this is about communication with your team, regularly checking in and making sure they understand the goals set, building them up and praising their achievements (including behaviour) and making sure you give them the feedback when the have done something wrong or delivered incorrectly. This may sound simple. Think about the Managers you have had that have done all 3 and the ones that have not its a great leveler.

Stephen C. Lundin , Harry Paul & John Christensen – FISH

This is one of my favourite culture books. I have used the Fish philosophy when building culture in many of my past teams. Some teams were established and performing but not well and some were in a bad way. The basic philosophy was bought about through a new leader interacting with staff at the Fish Market in Seattle. She was given a role to change a department know as the “Toxic waste dump” The 4 platform philosophies are;

Chose your attitude every day

Make someone’s day every day

Be Present

Have Fun

They may sound simple but requires a lot of guidance and continual practice. Is your team culture unpleasant? Is it know as the toxic waste dump in your organisation? Take a look, this will definitely make a difference to team culture !

I know how this set of philosophies can make that difference no matter the industry and organisation.

Tony Lendrum – The Strategic Partnering Pocketbook

I have been very lucky to have met and worked with Tony on numerous occasions. This book and methodology is based around the Supplier and Customer Dyad and the dynamics to get Win / Win outcomes and growth from your strategic partnerships.

The first key principle is to understand and map all your relationships. Not all relationships need to be strategic and there are very successful relationships that are tactical so you need to work out which ones you want to spend time on and implement a relationship program.

Once the relationships are mapped there are tools to understand where both organisation’s have the propensity to partner. Workshops are completed to agree the partnership programme with key actions and governance models enabling the delivery of shared value and growth.

I have used this methodology many times both as a supplier leading it with our key customers and as a customer leading our suppliers. There is a lot of talk about Supplier Relationship Management and Customer Relationship Management however my greatest success has come from using this methodology in all my strategic relationships.

The key take out is first understand the type of relationship you have and then discover where there is a propensity to partner to enable growth and create a win/win. If not aligned then maybe you should change! The fundamental outcome is that you have to be aligned and want the same thing out of the relationship / partnership.

P. Steele & Brian H. Court – Profitable Purchasing Strategies

This was a foundational book when I entered into my first Procurement and Supply Chain role over 15 years ago . It details the basics and tools that can be used to deliver end to end strategic procurement within an organisation. The case is made for purchasing to be viewed as an essential business process. Again, this book has a significant focus on the relationship dyad.

The 2 key tools and insights I gained were the Supplier Positioning Model- a modification on the Kraljic Matrix and the Supplier Preferencing Model providing insights on segmentation and management actions required to deliver the best value outcomes.

These 2 tools within a very detailed procurement book and guide are what I would call staples for any procurement practitioner. If you are not using a variation of these 2 by 2 matrices then you will not understand the value and behaviour / potential behaviour of your supplier base.

A highly recommended read for any procurement or supply chain practitioner.

Louise Hart – Procuring Successful Mega Projects

I was fortunate to work with Louise at Transpower ( the National Grid) in New Zealand. Louise has previously been involved in many mega Transport projects in both U.K and Sydney, all in the public sector and in the advent of Public Private Partnerships.

This book encapsulates the 30 years experience that Louise has gained across the Public and Private Sectors in large projects across different jurisdictions. Her legal beginnings has given her a great platform in understanding the basic needs of contracting practices and the need for clear objectives. I would like to thank her for mentioning me in her preface as we often discussed our common understanding of the end to end processes, experiences and issues that have arisen from procurement and contracting of projects.

The takeaways are succinctly put in chapter 19 A final Word;

Be clear in the objectives

Leave your brain switched on

Find the best people

Identify all of the scope

Allocate risk to people who know what to do with it

Design the right procurement process

Consult. Properly

Insist on good governance

Distinguish between price and value for money

Acknowledge your own fallibility

Colin Ellis – Culture Fix

Colin Ellis and Culture Fix are another author and book which has positively shaped my leadership career . Colin and I were fortunate to work together in the ICT department at Transpower in New Zealand ( The National Grid). Colin was Head of the Enterprise Project Office and we were both part if the ICT leadership team. His book was only published in 2020 and contains a real pragmatic view of what is culture and why culture is critical when building high performing organisations / teams. Colin’s leadership journey commenced about 20 years ago and he has used his experience and collated some great input from successful organisations across the world. The 2 big takeaways for me are;

Values and Behaviour

Values are an intrinsic part of culture creation when delivered with the Vision and Mission you set as a leader

Values must be lived and will require courage

Values should be specific to the organisation (not bland and generic)

Values should be used in the hiring process

Behaviour change is crucial for any kind of transformation

Knowledge of behaviour change is one thing, action and accountability quite another

Keeping secrets is bad for culture, even if no one knows

Frequently when you see things written down you know that they make common sense and think yep I get that. This is the beauty of great books and why so much time is spent to research and compile. Colin’s book is one of these books with many real examples, case study and quotes from CEOS and leaders of successful organisations. The book also has it reference’s tabulated against the sections of the book to easily find if you want to expand you knowledge in a specific area of culture.

Fiona and I also have a favourite quote from the book from the CEO of Airbnb Brian Chesky

” Culture is a thousand things a thousand times”

Michael Marquardt – Leading with Questions

Growing up and being a parent I am sure many of you would have had the experience with children that keep asking questions even after you have given them an answer. Constantly asking questions can often appear to be seen as frustrating for staff and colleagues. This book has a practical set of initiatives that can be used in leading organisations and staff . It starts by looking at the power of questions and how they can be used as management tools and culture builders. It gives a guide of how and when to ask questions when managing people, teams , solving problems and even developing strategy. My takeaway from this book is the power of questions to enable and build relationships. Here are some of the questions that empower relationships when managing people;

What can we learn from this?

Do you understand what I’m asking you to do?

How can I help you?

What’s next?

Where should we be placing our best energy?

What are we missing or forgetting?

How can we do it better next time?

What do you think?

What changes could we make to make your work-life better?

What would you do differently if you has my position?

Are you enjoying your work?

How can I improve my communication with you?

Malcolm Gladwell Outliers – The story of Success

Outliers explains why “the self-made man” is a myth and what truly lies behind the success of the best people in their field, which is often a series of lucky events, rare opportunities and other external factors, which are out of our control. However if you look at this summary you may think why has this part of my Top 10 leadership books. Within the detail there is clear evidence that to achieve mastery of anything it takes 10,000 hours of practice. This is basically 5 years.

Therefore the old adage ‘the harder I work the luckier I get’ is attributed to the number of hours I have practiced in that field and eventually reaching mastery. I’ve mapped my Rugby Union career from the date I got my break to play at elite level with Harlequins in London and the number of actual games I had played and practiced the skills. Prior to my breakthrough I was playing 3 games a week at school, club and county level and practicing 3 times a week for between 1-2 hours through this I had achieved mastery enabling me to be picked up at an elite level club. ( The harder I worked the luckier I got )

The basic premise is the more you do something the greater your experiences are and your ablity to second guess the next steps correctly almost become second nature.

My learning after 33 years of being a people leader is that experience allows you to deal with all eventualities when leading teams and people. This enables confidence and confidence along with trust are important charismatic characteristics in your leadership career!

An inspiring must read that might change your thought processes about success.

Daniel Pink – A whole New Mind

The tag line on the front cover is provocative and as a leader should entice you into reading this “Why Right – Brainers will rule the future”. If that is not enough to make you open the book read the back page tag line – “If its likely soon in China or India can do your work more cheaply than you can , or if a computer can do your job faster than you can , read this book”. The book was first published in 2005 so can also add Artificial Intelligence (AI) to this quote.

The book looks through history and explains why leaders in the past have been Left Brain Thinkers, MBAs were the most sought after qualification for CEOs and now computers can do all that left brain sequential and numbers stuff. Our growth in humanity has been to high concept and high touch, introducing abundance and automation and what that means for future leadership.

My insight is that Right Brain leadership will enable all our future organisations. The Masters of Fine Art will become the new MBA. People want stories, the reason why, concepts and ideas. Just look at how advertising has gone from formats that emphasise price reduction, save x, we are the cheapest etc to telling stories and beautiful images. One that has hit me recently is the beer advert by Heineken. Obviously there are issues with beer sales world wide and the move to more specialist brews, ready mixes and wine consumption growth. A new advert shows bar staff delivering a cocktail to a woman and the Heineken to the man in various situations. The powerful message in the story is when they swap glasses. The advert ends with the text “Women like Heineken too”

This is a clear example of what Daniel Pink has presented in his book.

Pink introduces the Six senses below;

Not just function but also DESIGN

Not just argument but also STORY

Not just focus but also SYMPHONY

Not just logic but also EMPATHY

Not just seriousness but also PLAY

Not just accumulation but also MEANING

Ken Blanchard & Renee Broadwell – Servant Leadership in Action

Well I have left what I think is one of the best leadership books to last.

Ken Blanchard opened up the leadership vision by introducing servant leadership in 2011 even though his books of the 90s he had hinted at the need to support your team. Blanchard believes that servant leaders are constantly trying to find out what their people need to perform well and to live according to their organisation’s vision. Rather than wanting people to please their bosses, servant leaders want to make a difference in their employees’ lives and in their organisations.

He basically tips the Autocratic Leadership Pyramid on it head with the team being at the top and the most important as they are closer to the customer in delivery of the organisation’s vision. The leader sits at the bottom of the pyramid supporting the team.

This has always been completely aligned to my leadership vision from the age of 24 and also as a captain of many Rugby Union sports teams. A leader or captain is a reflection of the team and the team performance. It does not matter how good you are as an individual if your team is not performing then you are not performing. The teams success is your success.

Here are 10 of the characteristics that make a great servant leader ;

Listening

Empathy

Healing

Awareness

Persuasion

Conceptualization

Foresight.

Stewardship

Commitment to the growth of people

Building community

Many leaders feel threatened by Servant Leadership and use hierarchy and role status to control. I have seen this many time throughout my career, and this is a reflection of the leader not being confident about their own position and capabilities. There is also this inherent fear that team members will take their own role which should be seen as a success rather than a failure. To me this is a very shortsighted leadership approach and eventually is flawed.

Being a servant leader is very time consuming especially in large teams. It takes time to understand each team member and requires input through one to one coaching. You are there to enable each member to achieve goals creating a high performing team and delivering organisational success. It is not for faint hearted and like culture with a play on the quote by the CEO of Airbnb Brian Chesky;

leadership is a thousand things a thousand times – supporting and enabling your team to win (achieving personal and organisational goals).

Its been a while so I think you may enjoy this blog

We talk a lot in the procurement world about ethical procurement and how important it is to all the buyers in the modern era. Provenance is an element that can assist with the transparency of how the goods and services are manufactured and delivered by a supplier from any Industry.

How does Provenance work and do we really care about this when we buy something?

Lets start with a definition – what is Provenance?

Provenance (from the Frenchprovenir, ‘to come from/forth’) is the chronology of the ownership, custody or location of a historical object.[1] The term was originally mostly used in relation to works of art but is now used in similar senses in a wide range of fields, including archaeology, paleontology, archives, manuscripts, printed books, the circular economy, and science and computing.

The primary purpose of tracing the provenance of an object or entity is normally to provide contextual and circumstantial evidence for its original production or discovery, by establishing, as far as practicable, its later history, especially the sequences of its formal ownership, custody and places of storage. The practice has a particular value in helping authenticate objects. Comparative techniques, expert opinions and the results of scientific tests may also be used to these ends, but establishing provenance is essentially a matter of documentation. The term dates to the 1780s in English. Provenance is conceptually comparable to the legal term chain of custody.

Provenance was designed to gain trust through authentication and transparency. Since the 19th Century it has been a key part of the art world both from an ownership and collection function. It is second nature for Museums, Galleries in the Art world and has expanded to other sectors within these markets.

Researching the provenance of paintings — The principles of archival provenance were developed in the 19th century by both French and Prussian archivists, and gained widespread acceptance on the basis of their formulation in the Manual for the Arrangement and Description of Archives by Dutch state archivists Samuel Muller, J. A. Feith, and R.

So how important is the adoption of Provenance in the Procurement and Supply Chain World?

Harvard that explains “the why as”

“The origins of a company’s products used to be pretty murky. Beyond the supply chain function, virtually no one cared. Of course, all that’s changed. Consumers, governments, and companies are demanding details about the systems and sources that deliver the goods. They worry about quality, safety, ethics, and environmental impact. Farsighted organizations are directly addressing new threats and opportunities presented by the question, “Where does this stuff come from?”

Remember the iPhone factories and suicides’ of staff, what about modern slavery and poor working conditions in the fast fashion industry to name a couple of relevant examples of why it is import to have transparency in our supply chains.

Safety has also been a criteria for Provenance in the supply chain.

Food safety has been see as high risk world wide due to many stores of contaminated products. Who can forget in late 1980s Bovine spongiform encephalopathy BSE or commonly know as Mad Cow disease in the U.K? I still cant give blood here in NZ!

New Zealand has a reputation for having rigorous food safety standards and high-quality produce. Consequently, there is a high risk of food fraud, and food contamination incidents around the world are driving the need to protect this reputation.

We are even more interested now on paddock to plate provenance of our food. A nice rack of lamb on are plate and I can hear someone thinking! Was it from a lamb that was fed on grass grown organically – without pesticides? Was it ethically slaughtered in an abattoir ? How was it package? ( no plastic ) and how was it transported? ( emissions ). Does the supermarket I bought it from pay the living wage?

Listen to this Radio New Zealand article about a Dunedin-based company Oritain uses chemical fingerprinting of produce to verify the origin of foods another form of provenance stamping.

We all know the issues about Bangladesh and fast fashion – This is a great article from NPR and another from NY times that really opened up the issues with fast fashion ethical manufacturing of fashion items and not only the conditions of workers but the impact the dumping of waste on our environment.

I hope you have enjoyed this quick insight – my aim is to give you some examples to read and enlighten you about how provenance has become one of the most important aspects of goods and services that we procure today. The Buyer is making decisions based on Ethical Sourcing! I think we do care about provenance and it will only increase.

With the advent of COVID 19 traceability in the supply chain has become a far more important exercise and topic not only due to risk of late or non delivery by many other factors either positive or negative. See the Boston Consulting Group model below and the many factors that could influence the supply chain;

Since the age of 18 I have been working and developing my leadership knowledge through practical experiences, professional courses, qualifications, books and the practical experience that comes from being part of a work based team. At the age of 24 I was given my first leadership role at British Telecom leading a team of over 20 people. Christmas 2020 has seen me reflect on my leadership journey and knowledge gained and implemented in many of my past teams and organisations. There are so many writers missing including Richard Branson, Sir Alex Ferguson, Jeffery Hiatt, Gwendoline Smith, Don Steinberg but I’ve selected the texts I often refer to with the most thumbed pages.

After an extraordinary year that I never thought I would experience and the impact of COVID19 I have summarised my key “takeaways” from each book. I know that when you get the chance to read some of these publications you’ll find many others. Let us kick off with the first book and enjoy.

Ken Blanchard & Spencer Johnson – the One minute manager

This book was designed for busy Managers and suggests that you spend 60 seconds per day; or at least per week (my thoughts) on each of the following;

a) Discussing and setting clear goals

b) Giving praise as feedback

c) Creating clarity and feedback when things require development (reprimands)

Basically this is about communication with your team, regularly checking in and making sure they understand the goals set, building them up and praising their achievements (including behaviour) and making sure you give them the feedback when the have done something wrong or delivered incorrectly. This may sound simple. Think about the Managers you have had that have done all 3 and the ones that have not its a great leveler.

Stephen C. Lundin , Harry Paul & John Christensen – FISH

This is one of my favourite culture books. I have used the Fish philosophy when building culture in many of my past teams. Some teams were established and performing but not well and some were in a bad way. The basic philosophy was bought about through a new leader interacting with staff at the Fish Market in Seattle. She was given a role to change a department know as the “Toxic waste dump” The 4 platform philosophies are;

Chose your attitude every day

Make someone’s day every day

Be Present

Have Fun

They may sound simple but requires a lot of guidance and continual practice. Is your team culture unpleasant? Is it know as the toxic waste dump in your organisation? Take a look, this will definitely make a difference to team culture !

I know how this set of philosophies can make that difference no matter the industry and organisation.

Tony Lendrum – The Strategic Partnering Pocketbook

I have been very lucky to have met and worked with Tony on numerous occasions. This book and methodology is based around the Supplier and Customer Dyad and the dynamics to get Win / Win outcomes and growth from your strategic partnerships.

The first key principle is to understand and map all your relationships. Not all relationships need to be strategic and there are very successful relationships that are tactical so you need to work out which ones you want to spend time on and implement a relationship program.

Once the relationships are mapped there are tools to understand where both organisation’s have the propensity to partner. Workshops are completed to agree the partnership programme with key actions and governance models enabling the delivery of shared value and growth.

I have used this methodology many times both as a supplier leading it with our key customers and as a customer leading our suppliers. There is a lot of talk about Supplier Relationship Management and Customer Relationship Management however my greatest success has come from using this methodology in all my strategic relationships.

The key take out is first understand the type of relationship you have and then discover where there is a propensity to partner to enable growth and create a win/win. If not aligned then maybe you should change! The fundamental outcome is that you have to be aligned and want the same thing out of the relationship / partnership.

P. Steele & Brian H. Court – Profitable Purchasing Strategies

This was a foundational book when I entered into my first Procurement and Supply Chain role over 15 years ago . It details the basics and tools that can be used to deliver end to end strategic procurement within an organisation. The case is made for purchasing to be viewed as an essential business process. Again, this book has a significant focus on the relationship dyad.

The 2 key tools and insights I gained were the Supplier Positioning Model- a modification on the Kraljic Matrix and the Supplier Preferencing Model providing insights on segmentation and management actions required to deliver the best value outcomes.

These 2 tools within a very detailed procurement book and guide are what I would call staples for any procurement practitioner. If you are not using a variation of these 2 by 2 matrices then you will not understand the value and behaviour / potential behaviour of your supplier base.

A highly recommended read for any procurement or supply chain practitioner.

Louise Hart – Procuring Successful Mega Projects

I was fortunate to work with Louise at Transpower ( the National Grid) in New Zealand. Louise has previously been involved in many mega Transport projects in both U.K and Sydney, all in the public sector and in the advent of Public Private Partnerships.

This book encapsulates the 30 years experience that Louise has gained across the Public and Private Sectors in large projects across different jurisdictions. Her legal beginnings has given her a great platform in understanding the basic needs of contracting practices and the need for clear objectives. I would like to thank her for mentioning me in her preface as we often discussed our common understanding of the end to end processes, experiences and issues that have arisen from procurement and contracting of projects.

The takeaways are succinctly put in chapter 19 A final Word;

Be clear in the objectives

Leave your brain switched on

Find the best people

Identify all of the scope

Allocate risk to people who know what to do with it

Design the right procurement process

Consult. Properly

Insist on good governance

Distinguish between price and value for money

Acknowledge your own fallibility

Colin Ellis – Culture Fix

Colin Ellis and Culture Fix are another author and book which has positively shaped my leadership career . Colin and I were fortunate to work together in the ICT department at Transpower in New Zealand ( The National Grid). Colin was Head of the Enterprise Project Office and we were both part if the ICT leadership team. His book was only published in 2020 and contains a real pragmatic view of what is culture and why culture is critical when building high performing organisations / teams. Colin’s leadership journey commenced about 20 years ago and he has used his experience and collated some great input from successful organisations across the world. The 2 big takeaways for me are;

Values and Behaviour

Values are an intrinsic part of culture creation when delivered with the Vision and Mission you set as a leader

Values must be lived and will require courage

Values should be specific to the organisation (not bland and generic)

Values should be used in the hiring process

Behaviour change is crucial for any kind of transformation

Knowledge of behaviour change is one thing, action and accountability quite another

Keeping secrets is bad for culture, even if no one knows

Frequently when you see things written down you know that they make common sense and think yep I get that. This is the beauty of great books and why so much time is spent to research and compile. Colin’s book is one of these books with many real examples, case study and quotes from CEOS and leaders of successful organisations. The book also has it reference’s tabulated against the sections of the book to easily find if you want to expand you knowledge in a specific area of culture.

Fiona and I also have a favourite quote from the book from the CEO of Airbnb Brian Chesky

” Culture is a thousand things a thousand times”

Michael Marquardt – Leading with Questions

Growing up and being a parent I am sure many of you would have had the experience with children that keep asking questions even after you have given them an answer. Constantly asking questions can often appear to be seen as frustrating for staff and colleagues. This book has a practical set of initiatives that can be used in leading organisations and staff . It starts by looking at the power of questions and how they can be used as management tools and culture builders. It gives a guide of how and when to ask questions when managing people, teams , solving problems and even developing strategy. My takeaway from this book is the power of questions to enable and build relationships. Here are some of the questions that empower relationships when managing people;

What can we learn from this?

Do you understand what I’m asking you to do?

How can I help you?

What’s next?

Where should we be placing our best energy?

What are we missing or forgetting?

How can we do it better next time?

What do you think?

What changes could we make to make your work-life better?

What would you do differently if you has my position?

Are you enjoying your work?

How can I improve my communication with you?

Malcolm Gladwell Outliers – The story of Success

Outliers explains why “the self-made man” is a myth and what truly lies behind the success of the best people in their field, which is often a series of lucky events, rare opportunities and other external factors, which are out of our control. However if you look at this summary you may think why has this part of my Top 10 leadership books. Within the detail there is clear evidence that to achieve mastery of anything it takes 10,000 hours of practice. This is basically 5 years.

Therefore the old adage ‘the harder I work the luckier I get’ is attributed to the number of hours I have practiced in that field and eventually reaching mastery. I’ve mapped my Rugby Union career from the date I got my break to play at elite level with Harlequins in London and the number of actual games I had played and practiced the skills. Prior to my breakthrough I was playing 3 games a week at school, club and county level and practicing 3 times a week for between 1-2 hours through this I had achieved mastery enabling me to be picked up at an elite level club. ( The harder I worked the luckier I got )

The basic premise is the more you do something the greater your experiences are and your ablity to second guess the next steps correctly almost become second nature.

My learning after 33 years of being a people leader is that experience allows you to deal with all eventualities when leading teams and people. This enables confidence and confidence along with trust are important charismatic characteristics in your leadership career!

An inspiring must read that might change your thought processes about success.

Daniel Pink – A whole New Mind

The tag line on the front cover is provocative and as a leader should entice you into reading this “Why Right – Brainers will rule the future”. If that is not enough to make you open the book read the back page tag line – “If its likely soon in China or India can do your work more cheaply than you can , or if a computer can do your job faster than you can , read this book”. The book was first published in 2005 so can also add Artificial Intelligence (AI) to this quote.

The book looks through history and explains why leaders in the past have been Left Brain Thinkers, MBAs were the most sought after qualification for CEOs and now computers can do all that left brain sequential and numbers stuff. Our growth in humanity has been to high concept and high touch, introducing abundance and automation and what that means for future leadership.

My insight is that Right Brain leadership will enable all our future organisations. The Masters of Fine Art will become the new MBA. People want stories, the reason why, concepts and ideas. Just look at how advertising has gone from formats that emphasise price reduction, save x, we are the cheapest etc to telling stories and beautiful images. One that has hit me recently is the beer advert by Heineken. Obviously there are issues with beer sales world wide and the move to more specialist brews, ready mixes and wine consumption growth. A new advert shows bar staff delivering a cocktail to a woman and the Heineken to the man in various situations. The powerful message in the story is when they swap glasses. The advert ends with the text “Women like Heineken too”

This is a clear example of what Daniel Pink has presented in his book.

Pink introduces the Six senses below;

Not just function but also DESIGN

Not just argument but also STORY

Not just focus but also SYMPHONY

Not just logic but also EMPATHY

Not just seriousness but also PLAY

Not just accumulation but also MEANING

Ken Blanchard & Renee Broadwell – Servant Leadership in Action

Well I have left what I think is one of the best leadership books to last.

Ken Blanchard opened up the leadership vision by introducing servant leadership in 2011 even though his books of the 90s he had hinted at the need to support your team. Blanchard believes that servant leaders are constantly trying to find out what their people need to perform well and to live according to their organisation’s vision. Rather than wanting people to please their bosses, servant leaders want to make a difference in their employees’ lives and in their organisations.

He basically tips the Autocratic Leadership Pyramid on it head with the team being at the top and the most important as they are closer to the customer in delivery of the organisation’s vision. The leader sits at the bottom of the pyramid supporting the team.

This has always been completely aligned to my leadership vision from the age of 24 and also as a captain of many Rugby Union sports teams. A leader or captain is a reflection of the team and the team performance. It does not matter how good you are as an individual if your team is not performing then you are not performing. The teams success is your success.

Here are 10 of the characteristics that make a great servant leader ;

Listening

Empathy

Healing

Awareness

Persuasion

Conceptualization

Foresight.

Stewardship

Commitment to the growth of people

Building community

Many leaders feel threatened by Servant Leadership and use hierarchy and role status to control. I have seen this many time throughout my career, and this is a reflection of the leader not being confident about their own position and capabilities. There is also this inherent fear that team members will take their own role which should be seen as a success rather than a failure. To me this is a very shortsighted leadership approach and eventually is flawed.

Being a servant leader is very time consuming especially in large teams. It takes time to understand each team member and requires input through one to one coaching. You are there to enable each member to achieve goals creating a high performing team and delivering organisational success. It is not for faint hearted and like culture with a play on the quote by the CEO of Airbnb Brian Chesky;

leadership is a thousand things a thousand times – supporting and enabling your team to win (achieving personal and organisational goals).

With perhaps the exception of the 1918 Influenza pandemic we have never before experienced a health crisis like COVID-19 in terms of scale, global reach, and impact to business.

Here in New Zealand where 95% of registered businesses are SME a lockdown of over 10 weeks has hit cash flows in various ways. Subsidies may have softened the blow and enabled organisations to keep trading but many have either gone into liquidation or have cut their costs through staff redundancies.

The resurgence of the virus in Auckland and new lockdown restrictions emanating from New Zealand largest city has increased anxiety and stress with many more businesses tipping over the edge into closure.

‘Cash is king’, an opt-touted phrase originated in 1988, following the ’87 global stock market crash. The term was coined by Pehr G. Gyllenhammar, who was at the time CEO of Swedish car group Volvo.

Many organisations operate with little or no cash reserves and the disruption zero cash for 10 to 12 weeks has caused truly highlights the tight rope many SMEs are walking week to week in New Zealand.

Payment terms and actual payment of invoices has been a huge challenge in many industries, just look at FMCG and some of the big brand supermarkets in the UK and Australia being dragged through the press for not paying their suppliers or lengthy delays in paying suppliers

Tesco knowingly delayed payments to suppliers

By Emma Simpson Business correspondent, BBC News

Image copyright GETTY IMAGES

Tesco “knowingly delayed paying money to suppliers in order to improve its own financial position”, the supermarket ombudsman has found.

The Grocery Code Adjudicator, Christine Tacon, said the supermarket seriously breached the industry’s code of conduct to protect grocery suppliers.

She found extensive evidence that Tesco had acted unreasonably when delaying payments to suppliers.

Coles to pay milk supplier $5.25m after allegedly failing to pass on full price increase

This article is more than 6 months old – ACCC says it was ‘fully prepared’ to take Coles to court over the allegations

Thu 5 Dec 2019 00.20 GMTLast modified on Thu 5 Dec 2019 00.22 GMT

Coles will pay one of its milk suppliers $5.25m after an investigation by the Australian Competition and Consumer Commission. Photograph: Bloomberg/Getty Images

Supermarket giant Coles has agreed to pay an extra $5.25m to one of its milk suppliers to settle a stoush with the consumer watchdog over whether it was passing all of a 10c a litre price increase on to dairy farmers.

Post COVID19 cash flow for many organisations is the difference between life and death. Prompt payment is the most important variable for SMEs who has seen revenues drop by up to 80%. With bills and staff to pay cutting the overheads to support a sustainable future becomes the number one priority. Everywhere you are seeing slogans to buy local, help stimulate the economy, support small businesses.

New Zealand Government has looked at bringing in legislation for prompt payment for suppliers as they understand this is key for many businesses in its survival even before COVID19

Government considering legislation to make sure small businesses are paid on time

7:31 am on 26 February 2020 The government’s looking at law changes to ensure small businesses are paid on time.

Small Business Minister Stuart Nash said he is willing to legislate, if necessary, to ensure payments within 20 days, with interest imposed for late payments.

He said prompt payment and cash flow are vital to small business survival, and having to wait as long as 90 days to get paid by big businesses is unacceptable

Construction SubcontractorsWednesday, 27 May 2020, 6:12 pm

Subcontractors will have greater certainty, more cashflow support and job security with new changes to retention payments under the Construction Contracts Act says Minister for Building and Construction, Jenny Salesa.

The changes include:

introducing a new offence and penalties for company directors and firms who don’t comply with their responsibilities,

strengthening how retention money is held to prevent firms from dipping in to retention money to use as working capital,

requiring those holding retention money to issue a transparency statement stating how much is being held and where

The New Zealand Government has implemented Construction Contracts Act in the construction sector after many large organisations have gone into liquidation and left multiple sub-contractors high and dry without any payment for work carried out.

WHAT IS PEPPOL?

PEPPOL stands for Pan-European Public Procurement Online. The network was established as a test project by the European Commission in in 2008. Organisations that are now connected to PEPPOL can exchange business documents, such as various electronic formats, through the highly secured and safe international network

PEPPOL is an international e-invoicing network that allows you to safely send e-invoices to companies and governments worldwide.

The NZBN government website published the diagram below that gives you a great overview of PEPPOL. The Australian and New Zealand governments have adopted the standard as they see this an enabler for prompt payments especially in the SME sectors of both countries.

Organizations that are now connected to PEPPOL can exchange business documents in various electronic formats, through the highly secured and safe international network. It’s a secure network connection that uses a message exchange to deliver documents including e-invoices from system to system. This makes the transaction robust and error free.

It is very similar to the initial days of email when ISPs were set up as message exchanges to convert the different standards connecting system to system via a standardised language. I here you say but we have this currently it’s called EDI. Traditionally Electronic data interchange EDI has developed many standards such as;

Some major sets of EDI standards:

The UN-recommended UN/EDIFACT is the only international standard and is predominant outside of North America.

The US standard ANSI ASC X12 (X12) is predominant in North America.

The TRADACOMS standard developed by the ANA (Article Number Association now known as GS1 UK) is predominant in the UK retail industry.

The ODETTE standard used within the European automotive industry

The VDA standard used within the European automotive industry mainly in Germany

HL7, a semantic interoperability standard used for healthcare data.

HIPAA, The Health Insurance Portability and Accountability ACT (HIPAA), requires millions of healthcare entities who electronically transmit data to use EDI in a standard HIPAA format.

IATA Cargo-IMP, IATA Cargo-IMP stands for International Air Transport Association Cargo Interchange Message Procedures. It’s an EDI standard based on EDIFACT created to automate and standardize data exchange between airlines and other parties.

NCPDP Script, SCRIPT is a standard developed and maintained by the National Council for Prescription Drug Programs (NCPDP). The standard defines documents for electronic transmission of medical prescriptions in the United States.

Edig@s (EDIGAS) is a standard dealing with commerce, transport (via pipeline or container) and storage of gas

EDI can be transmitted using any methodology agreed to by the sender and recipient, but as more trading partners began using the Internet for transmission, standardized protocols have emerged.

This includes a variety of technologies, including:

The challenge for suppliers and customers is all of the above! Which standard do I use?

How do I connect to the customer or suppliers system if I don’t have the standard that they have?

PEPPOL will become a global standard for the exchange of documents with the initial standards focused heavily on e-invoicing.

BENEFITS of PEPPOL

Tradeshift− a PEPPOL access point provider claim there are immediate cost savings when using the PEPPOL e-invoicing capability “The benefits from this kind of shift include process cost reductions of up to 75%, up to 40% reduction in support calls and up to 18% more invoices paid on time.”

Along with this is increased process efficiency, compliance and robustness with a reduction of errors. Once you are connected you an promulgate this out to all your suppliers/customers in an efficient and effective end to end solution.

Standards and standardisation is not new however when you have the backing of 2 Trans-Tasman governments with the New Zealand government publicly stating the need for prompt payments to support the economy even pre-COVID-19, adoption will be the key to rapid deployment and reduction in payment times.

Companies such as Xero have already deployed PEPPOL in their solution stack for e-invoicing.

CONCLUSION

PEPPOL uptake and the backing by both governments in ANZ should see the adoption rates of this standard increase exponentially over time. Getting back to the title and question it asks, many sectors in New Zealand have been hampered by long to no payment cycles from customers. PEPPOL will enable faster & more accurate payment and could stimulate post COVI19 recovery for businesses by increasing cash flow and reducing debt days.

However it is not the silver bullet and will require us all as purchasers to think about how we spend our hard earned dollar supporting our local businesses enabling them to climb out of what potentially could be a deep recession. If intent is good and organisations contract to have more prompt payment of invoices the cash circulating through our businesses will flatten the effect of COVID19.

Payment delays may still occur though if organisations do not have processes in place to approve invoices promptly. Receipting is always an issue. One common occurrence is the lack of escalation processes when delegated authorities are away on holiday, off sick or just too busy.

Accounts Payable teams insist on robust processes and easy access to systems that enable prompt approvals and electronic 3 way matching.

This is by no means was an exhaustive look at the emerging PEPPOL standard and I hope you enjoyed the little insight and slant of this blog. As always comments and feedback are greatly appreciated

This is a quick Leadership hack during a time of volatility, uncertainty , complexity and ambiguity in the world we are currently living in.

COViD 19 has really put a shot across the bows of the world we live in today and I don’t think things will ever be like what we have known in the times pre COViD.

Have you hear of Above and Belowthe line thinking? Are you a Above or Below the line thinker?

A simple leadership hack is depicted in the diagram below;

Above the line thinking is often associated with having and Open Mindset. At any point of time in your day, week, month, year, decade, life, you will be either living above the line or below the line.

The question you should ask all leaders along with yourself is, “Which side of the line are you or am I living on?”

Are you living above the line, at cause? Or are you living below the line, also known as living at effect of things that happen to you?

Above the line thinking is about being open and curious. I love the list of questions below taken from Peopleleaders.com.au on how open minded people bring their mindset into play

What are my responsibilities here?

How can I accept what’s happening without blaming someone else?

Where I can take ownership and accountability?

How did I contribute to this?

What could I be doing differently?

Where is my role in this situation?

How can I make a difference?

How can I be helpful and of service to someone else?

How can I cooperate?

How can I support?

How can I add value?

How can I involve the right people?

It is being able to respond effectively and usefully in any given situation. It’s about starting with an intention and then working out how you can actually bring it into play.

Below the line thinking is often called a closed mindset. Again People leaders have a really simple way of describing this type of behavior.

“When your thinking is below the line, you’re protecting and defending yourself either passively (not contributing at all), or aggressively (by attacking others). This type of thinking is about trying to avoid responsibility, criticism and loss of control”,

Blame

Denial

Excuses and justification

They’re wrong

It’s not my fault

It’s got to be my way

I don’t trust what they’re saying

I know this seems a simple solution in what at times can be a very complex set of circumstances that can cause the behavior associated with either being above the line or below the line. The first step is identifying which of the descriptors you tend to associate with the most. Self-awareness and reflection is the start of your journey. If you are not happy with the result then start the journey to change!

If you want to stop feeling Frustrated, Dissatisfied, Impatient, Suspicious, Resentful, Tense and full of Fear, just start dropping language such as Cant, Wont, Should, Must, No and replace with language that empowers is more inclusive eg:

Replacing ‘but’ with ‘and’

Using inclusive language like ‘us, we, ours’ instead of ‘you, them and they’

Solution or future-oriented language, e.g. ‘What would it look like if we…?’

Let’s get this thing moving!

It is time for our leaders to stop blaming others, denying that there is not a global pandemic and trying to find excuses of why things in their country, organisation, environment have got so bad.

What sort of leader do you want to follow and aspire to be?

One that takes ownership, is accountable and responsible for what is being done or one that constantly blames, denies and comes up with excuses.

In my post The Future of Supply chains post COVID-19, I advocated that post COVID-19 an action procurement and supply chain professionals should undertake is digitising and creating safe and secure analytics. The use and power of big data will be key in understanding your supply chain and managing risks.

Today’s businesses, especially large global enterprises have hundreds of separate applications and systems (i.e. ERP, CRM). Data crosses organisational departments or divisions and easily becomes fragmented, duplicated and most commonly out of date. When this occurs, answering even the most basic, but critical questions about any type of performance metric or KPI for a business accurately becomes a pain.

Access to data is increasing, however data is stored on many different systems and extraction has grown exponentially in complexity.

How complex can this be?

What data do I need?

How timely can I get access to it?

How can I present it in a way that is meaningful and easily understood?

Many of you have asked similar questions within your business environments, especially when presenting insights to executives and boards.

Procurement and Supply Chain Mega Trends

Lari Numminen, Chief Marketing Officer in his article “7 Megatrends for the Future of Procurement” highlights the combination of internal and external data sources as one of these Mega trends with many companies having detailed visibility on internal data, on costs, supplier contracts and so on. As more big data solutions emerge for external signals, like the weather, commodity prices, and other factors, co-founder of Sievo, Sammeli Sammalkorpi argues that a source of future competitive advantage will be the ability to combine internal and external data sources.

The EY article“Ten trends shaping the future of procurement” highlights that organizations will leverage internal and external data sources to better assess supplier risk. He stated that in the near future, most organizations will have a 360-degree view of suppliers through internal data, data from suppliers, market data and external data on suppliers’ performance (e.g., performance of suppliers with other organizations). This will not only provide historical data about supplier performance but will also enable organizations to accurately and holistically establish supplier risk profiles and to predict risk events.

Spend Matters cites Big Data and analytics as one of the 5 Mega Trends Reshaping the Supply Chain. Trend number 2 states that the chat will focus not just on analysing larger datasets but also the underlying requirements to do so — and the possibilities with Big Data approaches to procurement. (Hint: It’s anything but just expanding “spend analytics” to new areas.)

Finances online Jenny Chang published an article on the “14 Supply Chain trends for 2020: New predictions to watch out for”. The graph below illustrates clearly how data analytics has appeared as one of the priority technologies for the Supply Chain Industry.

Source: Finances online

The Link between MDM and the Supply Chain mega trend Big Data

Without…. getting answers to basic questions such as “who are our most profitable customers?”, “who are our key suppliers” and “who supplies them to create the products we receive?” “what product(s) have the best margins?” or in some cases, “how many employees do we have”? become tough to answer – or at least with any degree of accuracy.

The need for accurate, timely information is acute. As sources of data increase, managing it consistently and keeping data definitions up to date to enable all parts of a business to use the same information is a never-ending challenge.

Data analytics are one of the key Mega trends for Procurement and Supply Chain Management. COVID-19 has increased the hunger for information. Daily reports and updates on case numbers and mortality rates have been religiously watched by hundreds of millions of people globally.

Evidenced based decision making requires timely and accurate information. When managing risk in your supply chain, how many organisations truly have levels of data from every element of their high-risk suppliers?

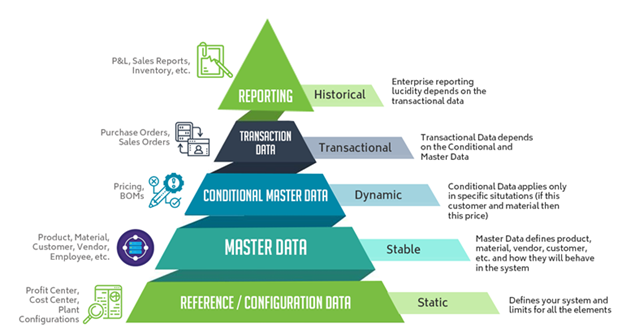

What is Master Data Management?

Some of you may wonder what Master Data Management is? Below is a quick snapshot and definition and why MDM is important. As always please contact me if you would like any more information on this technology.

Source: Duco Consultancy

Master data management is a method used to define and manage the critical data of an organisation to provide, with data integration, a single point of reference.

Master data represents the business objects that contain the most valuable, agreed upon information shared across an organisation. It usually covers relatively static reference data and not transactional data such as sales orders, stock etc.

The slide below highlights some of the opportunity costs of poor data management

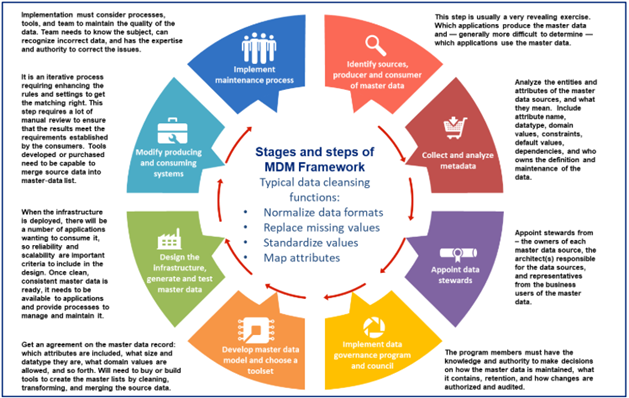

How do you implement Master Data Management?

Arvind Joshi, PMP Director – Data Management Lead at Scotiabank in his LinkedIn article has documented a useful overview of how you implement Master Data Management

Source: Linkedin

Implementing Master Data Management must be business led. It is not simply choosing a technology solution and supplier. The key steps in implementation are data profiling, understanding what data is important to the business and what the business currently collects across all its systems and databases. Data definition and prioritisation (the data to be kept and updated) are also keys steps in implementing MDM.

I cannot stress enough the importance of developing a data governance model and appointing a data steward and a governance council. It is pointless spending $Millions on technology if you do not maintain data quality.

Data quality management is as important as the data itself and if not maintained to the highest standards it could end up being out of date. Poor data can cost you millions as highlighted in the slide earlier.

Once you have completed the key steps above and the governance process is defined and architected then the data must be extracted from your existing systems cleaned and then loaded onto the solution chosen by your organisation.

Extracting the data from all the sources throughout your technology environment can be complex; however there are tools that can assist to help transform the data to your requirements and load into the system that you will maintain as your single source of truth.

Technology Providers

There are many technology solutions today to capture, present & report information on your important data across multiple domains and systems within an organisation. Often many large organisations have just grown organically. Acquisition has also added to the complexity of the technology environment. Access to data in complex IT topologies has challenged many experts.

For reference here is a list of some of the top technology suppliers of MDM solutions (forgive me if I have left some of you out);

Ataccama

Profisee

Talend Master Data Management

Orchestra Networks

SAS

SAP

Stibo Systems

Tibco

IBM

Agility Multichannel

Omni-Gen

Riversand

Oracle

VisionWare

Informatica 360

Enterworks

Gartner magic quadrant has more up to date information on each supplier that contributes to its publication. Please note that these are often not exhaustive. Add this tool to your set of tool when evaluating what is suitable for your organisation.

Supplier selection should be based on business led consultation and alignment with needs and expectations. There are some big differences and maturity between each solution. Understanding your current and future state requirements is paramount when making a technology choice.

Summary

All organisations will need to continually Improve their data insights to effectively manage their data. Peter Drucker is often quoted as saying “if you can’t measure it, you can’t manage it.” But it is more than just measuring today!

Big Data is used to create competitive advantage, alongside measuring, forecasting and risk management. The insights created are the fundamental elements of governance, leadership, strategy and operational intent.

MDM platforms draw information from multiple domains and departments and singles out the core data that administrators have determined is most relevant to the organisation. Users can then implement that data as they see fit, keep records of data history, and make projections based on findings.

The link with Data Analytics and Supply Chain Management be it risk, demand, supply and its importance in decision making should be obvious. Post COVID-19 the need for Procurement and Supply Chain professionals to collate the information and provide strategic and operational insight is essential for understanding our failings during the crisis.

Master Data Management is one of the silver bullets! (note: one of the silver bullets)

There are multiple solutions and getting it right first time is attributed to business led delivery. Use professionals to help you on this complex journey.

Data quality pro have a great “Beginners Guide to Master Data Management (MDM)” there is a link in my references below.

If you would like further information on how to deliver MDM and capabilities required Duco Consultancy ( https://www.ducoconsultancy.com ) are experts in delivery of the Technology solutions for MDM. Help with business cases and any information please send me an email at Mike@ducoconsultancy.com or mike.blanchard@xtra.co.nz

We are in extraordinary times and we will get through it. Yesterdays announcement of a further week in Lock down Level 4 and the 2 Weeks in Level 3 has given us some certainty in NZ to see the light at the end of the tunnel. It looks like we are on the right track to stamp out COVID 19 from the contribution of the courageous actions our government and our 5 million team. It will be a very long time until we realise if this was the correct course plotted by our country’s leadership.

Unfortunately, every decision in a crisis such as this comes at a cost. At what cost? We will start to see this over the next few months and the sage adage “Time will tell” truly applies.

I was thinking back to my childhood after a great discussion hosted by Nicola Willis the National MP and Steven Joyce the former Finance Minister on face book last night. The song When Will I See you again by the three degrees came into my head and reminded me of 1974 when I was in Berlin with my family. I will get back to that later.

We have some great people and minds in New Zealand! The debate obviously covered some of the Public Health v Economy compromise scenarios and how we can get back to seeing NZ economy being touted as the “rock star economy” it once was.

It is time to help all New Zealand Businesses by being innovative. The first thing we can do is to support them by purchasing locally (Buy Local). I have seen many innovative ways of purchasing goods that can either be delivered (contact less), in the future or start ups such as SOS café (David Downs – a truly remarkable fellow and innovator) where you purchase coffees and food vouchers now that you can expedite in the future post lock down.

The Tourism Industry is been one of the hardest hit Industries and we as New Zealanders have an obligation (once the local travel restrictions are off) to take our vacations in NZ . Let us support the recovery of this industry. I am not sure international travel will be opened for 6-12 months+ so it is a great opportunity to spend some time in our beautiful country catching sights that we either have never seen before or have not seen for quite a while again.

We cannot ignore all the people that have been doing it tough. My mother in law who is 82 is literally locked up on her own in her apartment at a retirement village and is not even allowed to have a drinks night with neighbours on the balcony that connects them all. She is not tech savvy and we have tried to walk her through video conferencing, but this has not worked. (This is Isolation). However, my nearly 2 year old granddaughter asks her parents every day to speak with grandma and granddad and although in isolation we get to have a virtual face to face chat which is an amazing way to stay connected (she even knows which button to press on the phone!).

So back to Berlin and the Three Degrees. In 1974 the Berlin wall was up and there were still many families that had been separated post war between East and West Germany. People had been shot from the East for trying to escape.

The Check point Charlie Museum is a great place to go and see the enormity of the issues these families faced. That was isolation in another time and country, and I am sure the families did not know when they would see their loved ones again.

We will get through this! We will be strong again and We all need to help each other get to the other side of COVID 19 by being kind and help build resilience.

The first 2 words of the song is Precious Moments. Take some time to share these precious moments with your family and friends (some of us may never have quite the same opportunity again). You will not have to wait forever for your hearts to be together and it is just the beginning.

Our hearts will be together — be safe — be kind — support each other

Kia Kaha New Zealand – The World — we have got this — so let us do this 😊

COVID19 has shown the world that we are as vulnerable as ever and the might of globalisation can in turn be our downfall.

Pandemic reporting internationally has turned the rhetoric of “supply chain/s” into a household phrase;

This current crisis is the quintessential example of the impact of supply chain disruption, that impact being rapid and global.

The effects are very real and compounded by the complexity of today’s global, inter-connected supply chains.

Empty shelves stand in the toilet paper aisle at a J Sainsbury Plc supermarket in Exeter, U.K., on … [+]

Toilet paper rarely makes headlines. No other commercial product save hand sanitiser and face masks have been more emblematic of coronavirus-inflicted global anxiety. Who would ever have imagined we would be fighting over the availability of the meagre little toilet roll? No other product so starkly highlights the different supply chain issues arising due to the current health crisis. After all, most experts agree that the rush to hoard toilet paper stems from an illogical anxiety. Remembering the days of ration books and quarantine our parents and grandparents will be laughing in their places or rest! I am sure the French with the bidets have wondered what all the fuss is about.

Food Supply Chain Coming into the COVID-19 Crosshairs

Grain markets this morning are mixed as disruptions in the global food supply chain challenge Plant 2020 headlines for attention from traders. Winter wheat prices are leading the complex as cooler temperatures in the Southern Plains could negatively impact a crop that’s just starting to get growing again. Outside markets are mostly higher as investors cheer on the net-new number of COVID-19 cases AND with deaths starting to slow, including in some of the worst-hit European countries, Spain, Italy, and France. As a reminder, this trading week is shortened as markets are closed on Friday in observance of Easter Good Friday!

What will happen to our hot cross buns? In New Zealand we already have a shortage of flour! The lockdown has taken us back to our grandparents days of home baking and the do it yourself (make it yourself) number 8 wire culture that home isolation has presented.

How quickly can we change the supply chain or remove the reliance of long distance supply lines by bringing it back on shore?

Coronavirus: White House rejects bipartisan bills to bring US medical supply chain back home

US Treasury Secretary Steven Mnuchin rejected the idea of using legislation to compel US medical supply companies to bring their manufacturing operations back home so Americans are less reliant on foreign countries for medical equipment during the coronavirus pandemic and future health crises.

Major disruption: How Covid-19 is affecting supply chains worldwide

With entire nations coming to a standstill to curb the rapid spread of the coronavirus, it will soon take its toll on supply chains around the world. The disrupted network of companies, factories and manufacturers could greatly affect the products we take for granted. Tech products, equipment, fashion, cars and other products are likely to have a stunted year ahead.

These are just a few snippets of news that we are exposed too currently on a daily basis constantly front and centre.

There is some COVID19 News out there that is also quite inspiring! Once again this highlights the way that we as human beings can adapt under a crisis;

Mercedes F1 team

The designs of a new breathing aid developed by engineers at the Mercedes F1 team, University College London (UCL), and clinicians at UCL Hospital have been made freely available to support the global response to Covid-19. It’s the latest development in Formula 1’s Project Pitlane effort to help fight coronavirus

Cumbrian oil services firm ‘ready to make 2,000 ventilators a week

A Cumbria-based offshore oil and gas services company has said it is ready to produce 2,000 ventilators a week to join the national effort to produce tens of thousands of machines to treat coronavirus patients.

James Fisher & Sons said it had sent a base model of its non-invasive InVicto system to the UK’s Medicines and Healthcare products Regulatory Agency (MHRA) for testing. If approved, the company said it could produce 2,000 a week.

The James Fisher ventilators are not designed for intensive care use, but the company said they can be used to relieve pressure on ICU beds by providing breathing support in “pre-critical temporary wards or care homes”

Head-lice drug gives scientist hope in fight against Covid-19

A cheap, widely used anti-parasite medication used to treat head lice killed Covid-19 cells in a petri dish and Aussie researchers hope to start human trials in a month.

Dr Kylie Wagstaff from the Biomedicine Discovery Institute at Monash University who carried out the study found Ivermectin began to kill Sars-COV-2 cells that cause Covid-19 in a petri dish within 24 hours.

Within 48 hours “we could prevent all replication of the virus in the cells,’ she said.

The study has been published online in the journal Antiviral Research.

Because the drug is already safely used in humans to treat parasites like head lice, River Blindness and scabies, it won’t be necessary to undertake lengthy animal studies and human clinical trials can be fast tracked on Covid-19 patients

James Dyson Designed a Ventilator in 10 days. Now He’s Making 15,000 to Fight Covid-19

The billionaire’s eponymous company plans to make 10,000 devices for the UK and 5,000 for international donation.

In an effort to combat the fast-moving spread of coronavirus, brands from every industry and country are pitching in to help. In France, LVMH is making hand sanitizer; in Italy, Gucci is making face masks; and, in the UK, Dyson is now making ventilators.

Best known for its vacuum cleaners and high-end fans, the British home electronics giant‘s founder, Sir James Dyson, said he has designed a new ventilator that can help ease shortages in his home country, according to CNN. The company now intends to produce 10,000 devices for the country’s National Health Service over the next month.

NZ volunteers pitch in to make thousands of face shields

This COVID business brings out the worst and best in people. Yesterday we saw the worst, today the best. The generosity of strangers: 3D printers have started printing free face shields for front-line medical practices, as there is a world-wide shortage, and they are being reserved for hospital use (We had none)